Current Revenues

The Commonwealth plans to raise $486 billion in 2018-19, and $2,105 billion over the forward estimates. There are recent indications it may raise more than this without changing policies.

Of this total 93% - or $452 billion – represents taxation, with the balance made up of sales of goods and services, dividends, interest and sundry other items of non-taxation revenue.

So tax is where the action is.

And just three taxes, personal income tax, company tax and the GST make up 83% of all taxation revenue in 2018-19. Meaningful tax reform is inconceivable without changing these taxes. That is not to say that changing other taxes should not be ruled out; quite the contrary. As Dr Ken Henry argued in his 2009 report, the efficiency of having hundreds of small taxes often on narrow and volatile bases is not perhaps the smartest way to collect revenue efficiently, effectively and fairly.

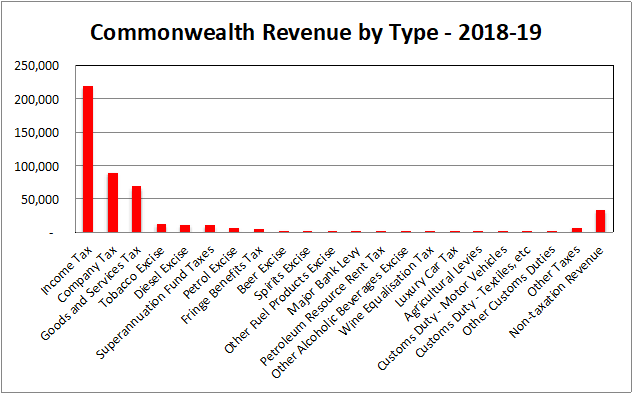

The chart shows the major items of revenue in the 2018-19 Commonwealth Budget.

Budget Paper No 1 2018-19, Statement 5, Table 7, p. 5-17

This is not the whole story, however. There are also tax expenditures – an economists way of saying that Governments also choose to forgo collecting some taxes they otherwise would. These could be exceptions to general principles of taxation, such as not applying capital gains tax to the family home, or not including family tax benefit or compensation payments in taxable income. There are even some negative tax expenditures – where Governments choose to apply taxation over and above normal levels – smokers bear the brunt of this, though there are other examples. Tax expenditures are highly contentious, and well worth considering in any program of tax reform. The Budget Test includes a number of them – primarily related to the GST – and I hope to add more later.

The revenue collected – and not collected - by the Commonwealth is determined for the most part by the parameters set in legislation and regulation and prevailing economic conditions.

There are important connections and feedback loops between most taxes, and between taxes and expenses, and it is important to understand that the models here take account only of the first round effects of changes you choose to make. The more important second round effects, though not modelled, are however pointed out and you should consider them when looking at the overall impact of the changes you propose to make.

For example:

- Increasing income taxes reduces household income, and therefore household spending and thereby GST receipts.

- Applying the GST to education will dampen demand for private education, and will thereby increase the requirement for the Commonwealth – and more so the States – for spending on public education.

- Decreasing company taxes will increase income tax and superannuation tax collections – as imputation credits will be lower.

- Changing fuel and alcohol excises will vary the GST collections associated with those products.

It is possible to throw one’s hands in the air and say this is all too hard.

It is also possible to use the models as intended, and to think carefully about what second and third round effects there might be, and to form views about what might and might not be good policy.

A model, no matter how complex and well constructed is only an imperfect tool, and not a substitute for thought.